Retirement Transition Planning: What Changes When Work, Paychecks, and Benefits End

Retirement is a major financial transition. It is not only a question of whether someone has saved enough money.

When employment ends, several systems may change at the same time. The paycheck may stop. Employer benefits may change. Retirement accounts may need review. Life insurance may end or reduce. Tax withholding may need adjustment. Estate documents and beneficiary designations may need to be revisited.

This article is designed to help organize the major planning questions that can come up before retiring from an employer. It is educational only and is not intended to recommend a specific retirement date, Social Security claiming strategy, rollover, insurance decision, investment strategy, tax election, or legal action.

Retirement transition planning is about organizing what changes when work, paychecks, employer benefits, and workplace defaults no longer operate the same way.

Why Retirement Transition Planning Matters

During working years, many financial decisions are built into the employer system. Payroll provides income. Benefits enrollment provides insurance options. Retirement contributions may happen automatically. Taxes may be withheld from paychecks. Beneficiaries may be attached to employer-provided accounts and policies.

When work ends, that system changes. Some decisions may have deadlines. Other decisions may not be urgent, but they may still affect future income, taxes, insurance coverage, estate documents, and account organization.

The purpose of a retirement transition review is to separate the immediate decisions from the longer-term planning questions.

Common retirement transition questions include:

- What income replaces the paycheck?

- What expenses continue, change, or disappear?

- What employer benefits end at retirement?

- What benefits may continue?

- What happens to the workplace retirement plan?

- When should Social Security timing be reviewed?

- Are pension options available?

- What happens to employer-provided life insurance?

- How should health coverage and Medicare timing be reviewed?

- Are beneficiaries current?

- Do estate documents still match the household situation?

- What tax questions should be coordinated with a tax professional?

Retirement Is More Than an “Enough Money” Question

Many people approach retirement by asking one question: “Do I have enough?”

That is an important question, but it is not the only one. A household may also need to review how income will be created, how taxes may be managed, what insurance coverage changes, how accounts are coordinated, and whether spending reflects what actually matters to the household.

Retirement planning often becomes clearer when the conversation moves from a single account balance to the full financial picture.

A retirement transition review may include:

- Monthly income needs

- Essential and discretionary expenses

- Emergency reserves

- Employer benefit end dates

- Life insurance and protection planning

- Retirement account structure

- Social Security timing questions

- Pension options, if available

- Taxable, tax-deferred, and tax-free accounts

- Required minimum distribution questions

- Beneficiary designations

- Estate planning documents

For related cash flow planning, see Cash Flow Management: Creating a Personal Cash Flow Statement.

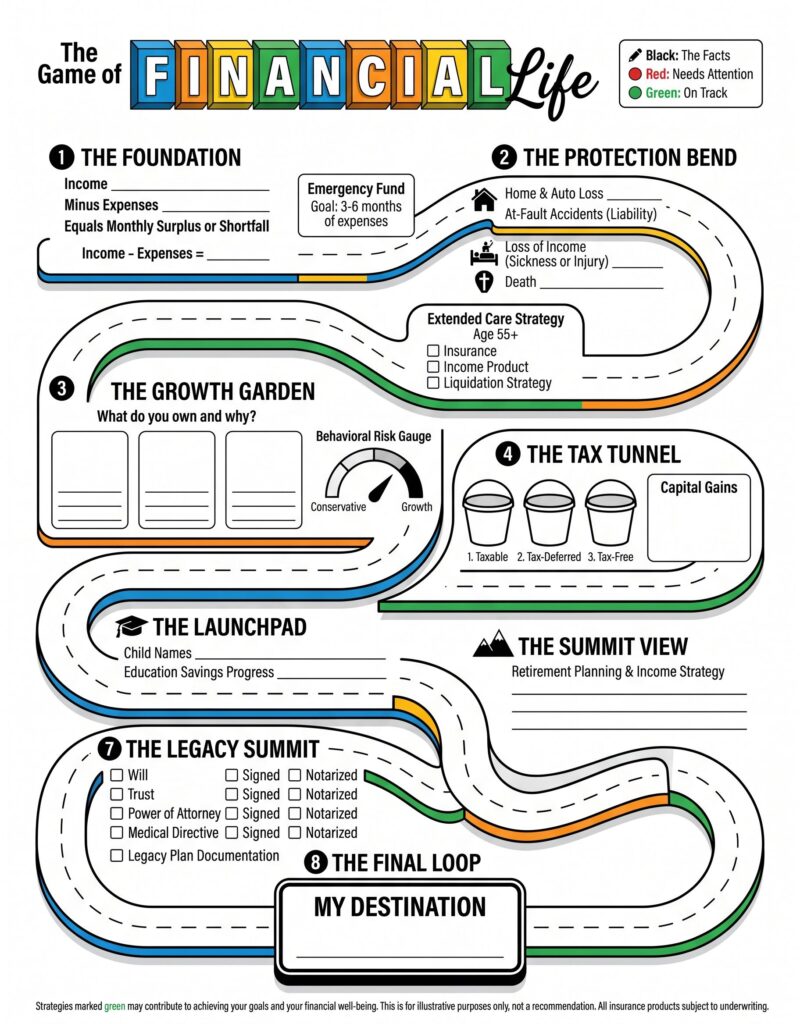

How Salt Lake Financial Planning Organizes Retirement Transition Questions

At Salt Lake Financial Planning, retirement transition planning is often organized through a broader Financial Life Framework. In planning conversations, this may be shown visually as the Game of Financial Life because it helps make a complex financial picture easier to navigate.

The purpose of the framework is not to make every decision at once. It is to organize the major areas that may need review before and after work ends.

The framework reviews several connected areas:

- The Foundation: income, expenses, emergency fund, and cash flow

- The Protection Review: insurance coverage and household risks

- The Growth Garden: investments, account structure, and risk tolerance

- The Tax Tunnel: taxable, tax-deferred, and tax-free accounts

- The Launchpad: retirement planning, education goals, and future income needs

- The Summit View: retirement income strategy and timing decisions

- The Legacy Summit: estate documents, beneficiaries, and legacy planning

- The Final Loop: goals, values, family priorities, and next questions

A retirement transition can affect the foundation, protection, investments, taxes, retirement income strategy, and estate flow of the household.

Start With the Foundation: Cash Flow After the Paycheck

The first retirement transition question is usually cash flow.

Before leaving work, it is useful to understand what it costs to maintain the current household lifestyle, which expenses may change, and what income sources may be available after employment income stops.

Foundation questions to review:

- What is the current monthly income?

- What is the current monthly spending?

- Which expenses are essential?

- Which expenses are discretionary?

- What expenses may decrease after retirement?

- What expenses may increase after retirement?

- What spending reflects the household’s actual values?

- What spending may be leakage?

- How much emergency reserve is available?

- How much monthly income is needed to support the desired lifestyle?

Retirement income planning should include both regular monthly expenses and irregular expenses such as home repairs, vehicle replacement, travel, family support, healthcare costs, taxes, and insurance premiums.

For more on retirement cash flow, see How Long Will My Savings Last in Retirement? and Retirement Portfolio Longevity Calculator: Planning Your Cash Flow.

Review What Retirement Should Actually Look Like

Retirement is not the same goal for every household.

For some people, retirement means leaving work completely. For others, it means working part-time, consulting, volunteering, helping family, traveling, spending more time outdoors, starting a small business, or simply having more control over time.

Before reviewing accounts and benefits, it can help to define what retirement is supposed to support.

Lifestyle questions to review:

- What would make retirement feel successful?

- What activities should retirement make more possible?

- Will work stop completely or continue in a smaller way?

- Will the household stay in the current home?

- Will travel, hobbies, or family support become larger expenses?

- Are adult children or grandchildren part of the financial picture?

- Is charitable giving or community involvement part of the goal?

- What expenses are actually meaningful?

- What expenses could be reduced without reducing quality of life?

- What would make retirement feel too constrained?

These questions matter because the retirement income plan should support the life being planned, not just a number on a statement.

Review Retirement Income Sources

After the paycheck ends, income may need to come from several sources.

Common sources may include Social Security, employer retirement plans, IRAs, pensions, taxable investment accounts, annuities, business income, rental income, part-time work, or other household assets.

Income sources to review:

- Social Security benefits

- Pension income, if available

- 401(k), 403(b), 457(b), or other employer retirement plans

- Traditional IRA accounts

- Roth IRA accounts

- Taxable investment accounts

- Annuity income, if applicable

- Business income

- Rental income

- Part-time employment or consulting income

- Cash reserves

For each income source, review:

- When income may begin

- Whether income is taxable

- Whether income is fixed or variable

- Whether income continues for a spouse or beneficiary

- Whether inflation adjustments apply

- Whether there are surrender charges, restrictions, or penalties

- Whether required distributions may apply later

- How the income source fits with other household income

For related retirement income calculators, see How Much Monthly Income Will My 401(k) Provide in Retirement? and IRA Retirement Income Calculator: Optimizing Your Withdrawals.

Review Social Security Timing Questions

Social Security is often one of the major retirement transition decisions.

Benefits may be available before full retirement age, at full retirement age, or later. Starting benefits early can reduce the monthly benefit. Delaying beyond full retirement age can increase the monthly benefit up to age 70.

The Social Security Administration provides information about early retirement reductions and delayed retirement credits. Review the rules carefully before making a claiming decision.

Social Security questions to review:

- What is the estimated benefit at different ages?

- What is full retirement age?

- Is the household relying on one benefit or two?

- Are spousal benefits relevant?

- Are survivor benefits relevant?

- Will employment income continue?

- How might benefits be taxed?

- How does Social Security coordinate with pension income?

- How does Social Security coordinate with retirement account withdrawals?

- What happens if one spouse dies first?

For general information, visit the Social Security Administration page on retirement age and benefit reductions.

For related SLFP content, see Social Security Planning: Key Questions Before Claiming Benefits and Social Security Taxation: How Much of Your Benefit Is Taxable?.

Review Pension Options, If Available

Some retirees have a pension or defined benefit plan through an employer.

Pension elections can involve long-term decisions. In some cases, choices may be difficult or impossible to change after benefits begin. Review the plan documents carefully and ask the plan administrator questions before making an election.

Pension questions to review:

- When can benefits begin?

- What is the normal retirement date?

- Is there an early retirement reduction?

- Is a lump-sum option available?

- What monthly payout options are available?

- Is there a single life option?

- Is there a joint and survivor option?

- Is there a period certain option?

- Are cost-of-living adjustments available?

- How would the decision affect a spouse or beneficiary?

- What tax withholding options are available?

- What is the election deadline?

The pension decision should be reviewed alongside household income needs, spouse or partner needs, other assets, health considerations, estate planning goals, and tax questions.

For related pension planning content, see Pension Planning: Joint Survivor vs. Single Life Payouts and Lump Sum vs. Ongoing Payments: Retirement Payout Questions to Review.

Review Employer Retirement Plans

Before retiring, review any employer-sponsored retirement plan such as a 401(k), 403(b), 457(b), SIMPLE IRA, or other workplace plan.

An employer retirement plan may have several choices after employment ends. The available options depend on the plan rules, account type, balance, age, employment status, and tax situation.

Employer retirement plan items to review:

- Current account balance

- Pre-tax balances

- Roth balances

- After-tax balances, if applicable

- Employer stock, if applicable

- Outstanding plan loans

- Investment options

- Fees and expenses

- Withdrawal options

- Installment payment options

- Rollover options

- Required minimum distribution rules

- Beneficiary designations

Required minimum distribution rules should also be reviewed. The IRS states that required minimum distributions generally begin at age 73 for many retirement accounts, though workplace plan rules and ownership status may affect timing.

For general IRS information, see IRS Required Minimum Distribution FAQs.

For related SLFP content, see RMD Calculator: Planning Your Required Minimum Distributions and Roth vs. Traditional 401(k): Strategic Tax Decisions for High Earners.

Review Old 401(k), IRA, and Rollover Questions

Retirement often raises the question of what to do with an employer retirement plan after employment ends.

Common options may include leaving assets in the existing employer plan, rolling assets into a new employer plan if available and permitted, rolling assets into an IRA, or taking a distribution. Each option may have different investment choices, fees, services, creditor protection rules, tax treatment, and administrative requirements.

This article does not recommend one option over another. The appropriate choice depends on the plan, account type, household circumstances, tax status, service needs, and long-term planning goals.

Rollover and account organization questions to review:

- What options does the current employer plan allow?

- What investment options are available inside the plan?

- What fees or expenses apply?

- Are Roth and pre-tax balances tracked separately?

- Is there an outstanding plan loan?

- Would an IRA provide different investment options or services?

- Would a new employer plan accept rollovers?

- How would a distribution be taxed?

- Are required minimum distributions relevant?

- Are beneficiaries current?

- Would consolidating accounts improve organization?

For more detail, see What to Do With an Old 401(k) After Leaving a Job.

If you are trying to locate accounts from prior employers, see How to Find Old 401(k) Accounts.

For general IRS rollover information, see Rollovers of Retirement Plan and IRA Distributions.

Review Tax Positioning Before and After Retirement

Retirement may change the household tax picture.

Income may shift from wages to Social Security, pensions, retirement account withdrawals, investment income, annuity income, business income, rental income, or other sources. Tax withholding may also need to be reviewed because payroll withholding may no longer be the primary tax payment method.

Tax questions to review with a tax professional:

- How will taxable income change in the retirement year?

- Will final wages, bonuses, severance, or PTO affect the tax year?

- How will pension income be taxed?

- How will Social Security benefits be taxed?

- How will retirement account withdrawals be taxed?

- Are Roth withdrawals available?

- Are taxable investment accounts creating capital gains?

- Are required minimum distributions relevant now or later?

- Should tax withholding or estimated payments be reviewed?

- Are charitable giving strategies relevant?

- Are Roth conversion questions worth discussing?

Tax planning should be coordinated with a qualified tax professional.

For related SLFP content, see Taxable vs. Tax-Advantaged: Optimizing Your Investment Location, Roth IRA Conversions: Is Converting Worth the Tax Bill?, and Taxes and Inflation: Retirement Planning Questions to Review.

Review Health Insurance and Medicare Timing

Health insurance is one of the most important transition items before leaving work.

If retirement begins before Medicare eligibility, review options such as spouse or partner coverage, COBRA, marketplace coverage, retiree health coverage, or other available coverage.

If Medicare is part of the transition, review enrollment timing carefully. Medicare states that the 8-month Special Enrollment Period to sign up for Part B starts when a person stops working, even if COBRA or other non-Medicare coverage is chosen.

Health coverage questions to review:

- When does employer health coverage end?

- Is retiree health coverage available?

- Is spouse or partner coverage available?

- Is COBRA available?

- What is the COBRA cost?

- Is marketplace coverage relevant?

- When should Medicare Part A and Part B be reviewed?

- Is prescription drug coverage changing?

- Are dental, vision, and hearing benefits changing?

- How does health coverage affect HSA eligibility?

- Who should be consulted for Medicare-specific guidance?

For general Medicare information, visit Medicare: When Can I Sign Up?.

For COBRA information, the U.S. Department of Labor provides a resource on COBRA Continuation Coverage.

Salt Lake Financial Planning does not provide Medicare plan selection advice. Medicare questions should be reviewed with Medicare resources, a Medicare professional, or the appropriate plan provider.

Review HSA and FSA Accounts

Health Savings Accounts and Flexible Spending Accounts may need special attention during a retirement transition.

An HSA may remain available after retirement, but future contribution eligibility depends on health coverage and Medicare status. FSA balances may also have reimbursement deadlines or plan-specific rules.

HSA and FSA questions to review:

- What is the current HSA balance?

- Are future HSA contributions allowed?

- Will Medicare enrollment affect HSA contribution eligibility?

- Are there employer HSA contributions still expected?

- What is the current FSA balance?

- What expenses are eligible for reimbursement?

- What reimbursement deadlines apply?

- Does a dependent care FSA apply?

- What records should be retained?

Review the specific employer plan documents before making HSA or FSA decisions.

Review Employer-Provided Life Insurance

Many employees have group life insurance through work.

At retirement, employer-provided life insurance may reduce, end, continue, or become available through portability or conversion options. The specific rules depend on the employer plan and insurance contract.

Life insurance questions to review:

- How much employer-paid life insurance is currently in place?

- Is supplemental life insurance in place?

- Is spouse or dependent coverage included?

- When does coverage end or change?

- Does coverage reduce at retirement?

- Are portability options available?

- Are conversion options available?

- What deadlines apply?

- How would the cost change?

- Are individual life insurance policies already in place?

- Are beneficiaries current?

- Does the household still have a coverage gap?

For more detail, see Life Insurance After Leaving a Job: Portability vs. Conversion.

For broader planning education, see Life Insurance Planning: Protecting Your Family’s Financial Future and Life Insurance Rates by Age.

Review Disability and Long-Term Care Planning

Disability coverage may become less relevant after retirement if employment income is no longer the primary income source. However, long-term care planning may become more important as retirement begins.

Extended care planning should be reviewed as part of the broader protection picture, not as a product decision.

Protection questions to review:

- Does disability coverage end at retirement?

- Does any employer-provided coverage continue?

- Is long-term care insurance already owned?

- Is hybrid life and long-term care coverage already owned?

- What care preferences does the household have?

- Is family caregiving part of the expectation?

- What legal documents would support care decisions?

- How would care costs affect the retirement income plan?

For related planning education, see Long-Term Care Planning: Managing the Cost of Assisted Living and How Much Disability Insurance Do I Need?.

Review Estate Planning and Beneficiaries

Retirement is a good time to review estate planning documents and beneficiary designations.

Employer retirement plans, IRAs, life insurance policies, bank accounts, investment accounts, and transfer-on-death designations may all have beneficiary information attached to them. These designations should be reviewed directly.

Estate and beneficiary items to review:

- Will

- Trust, if applicable

- Financial power of attorney

- Medical power of attorney

- Advance healthcare directive

- Employer retirement plan beneficiaries

- IRA beneficiaries

- Life insurance beneficiaries

- Bank and investment account beneficiaries

- Transfer-on-death designations

- Executor, trustee, and agent appointments

- Legacy planning documents

Do not assume a will or trust automatically updates retirement account beneficiaries or life insurance beneficiaries. Beneficiary designations should be reviewed directly with the account custodian, plan administrator, or insurance company.

For related SLFP content, see Your Estate Plan May Have a Hidden Gap: Why Beneficiary Reviews Matter and Wills and Trusts Educational Seminar.

Estate planning questions should be reviewed with a qualified estate planning attorney.

Retirement Transition Questions to Ask HR

Before the final day of work, it can help to ask the employer or benefits department direct questions.

Questions to ask HR or the benefits department:

- When does health coverage end?

- Is retiree health coverage available?

- When will COBRA information be provided?

- What happens to group life insurance?

- Is life insurance portability or conversion available?

- Does disability coverage end at retirement?

- What happens to unused PTO or vacation time?

- Are there bonus, commission, or incentive compensation issues?

- Are there pension election deadlines?

- What happens to stock compensation or deferred compensation?

- Are there retirement plan loan issues?

- What documents should be retained after retirement?

Retirement Transition Documents to Gather

A retirement transition review is easier when the major documents are available in one place.

Useful documents may include:

- Most recent employer benefits guide

- Retirement plan statement

- Pension estimate, if applicable

- Social Security estimate

- Life insurance summary

- Health insurance summary

- COBRA notice, if applicable

- HSA or FSA statement

- Deferred compensation statement, if applicable

- Stock compensation details, if applicable

- Recent tax return

- Recent paystub

- Estate planning documents

- Beneficiary confirmations

- List of financial accounts

- List of debts

- Monthly spending estimate

Common Retirement Transition Mistakes

Retirement decisions can be delayed, rushed, or made in isolation. A review process can help organize the questions before decisions become scattered across multiple providers, accounts, and documents.

Common mistakes include:

- Assuming employer benefits continue unchanged after retirement

- Ignoring group life insurance changes

- Leaving an old 401(k) unattended for years without reviewing the options

- Making pension decisions without reviewing survivor needs

- Claiming Social Security without reviewing household income needs

- Forgetting to update beneficiaries

- Not coordinating tax withholding after the paycheck stops

- Underestimating irregular expenses in retirement

- Spending in ways that do not match stated priorities

- Reviewing investments without reviewing cash flow, taxes, insurance, and estate documents

What This Review Does Not Replace

A retirement transition review can help organize financial questions, documents, and planning priorities. It does not replace the role of other professionals or plan-specific resources.

Depending on the issue, additional input may be needed from:

- Human resources

- Employer benefits department

- Retirement plan administrator

- Tax professional

- Estate planning attorney

- Medicare professional or Medicare resources

- Insurance carrier

- Payroll department

The purpose is to identify the right questions and coordinate the planning conversation, not to replace plan documents, legal advice, tax advice, Medicare advice, or employer-specific guidance.

Related Job Transition Resources

- Job Transition Financial Planning: What to Review When You Leave, Lose, Retire, or Change Jobs

- New Job Benefits Checklist: What to Review Before You Enroll

- Laid Off? A Financial Checklist for the First 30 Days After Job Loss

- What to Do With an Old 401(k) After Leaving a Job

- Life Insurance After Leaving a Job: Portability vs. Conversion

Additional Retirement Planning Resources

- How Long Will My Savings Last in Retirement?

- Will My Retirement Savings Run Out?

- How Much Do I Need to Save for Retirement?

- Social Security Income Calculator

- Pension Payout Options Calculator

- RMD Calculator: Planning Your Required Minimum Distributions

- 2026 URS Retirement Roadmap: Utah Retirement Systems

- 403(b) Accumulation: Retirement Planning for Utah Public Employees

- 457(b) Accumulation: Deferred Compensation in Utah

Review Retirement Transition Questions

Retirement transition planning does not need to start with a product decision or a recommendation. It can start by organizing the facts.

Bring employer benefit information, retirement account statements, pension estimates, Social Security estimates, insurance summaries, tax documents, estate documents, and questions that need to be reviewed.

Educational Disclosure

This material is for educational purposes only and is not intended as individualized financial, tax, legal, investment, retirement, health insurance, Medicare, or insurance advice. Employer benefits, retirement plans, insurance options, tax rules, Social Security rules, Medicare rules, and enrollment deadlines vary by plan and individual circumstances. Review your specific plan documents and consult the appropriate professional before making decisions.

Dallas Price is a Financial Planner and offers securities and investment advisory services through LPL Enterprise (LPLE), a Registered Investment Advisor, Member FINRA/SIPC, and an affiliate of LPL Financial.

LPLE and LPL Financial are not affiliated with Salt Lake Financial Planning.