A job transition can change more than your paycheck.

Whether you are starting a new role, retiring from an employer, leaving a company, or dealing with a layoff, your job may be connected to several parts of your financial life. Employer benefits, retirement accounts, life insurance, disability coverage, health coverage, tax withholding, beneficiaries, and household cash flow may all be affected.

This guide is designed to help organize the major financial questions that can come up during a job transition. It is not intended to recommend a specific product, rollover, insurance decision, tax strategy, or benefit election.

A job transition is not just a paperwork event. It can affect the foundation, protection, investments, tax positioning, retirement income strategy, and estate flow of the household.

Why Job Transitions Create Financial Planning Questions

For many households, an employer provides more than income. The employer may also provide access to retirement savings, health coverage, life insurance, disability insurance, legal benefits, HSA or FSA accounts, pension information, and payroll tax withholding.

When employment changes, some benefits may end, some may continue, and some may require action within a limited window. Other decisions may not be urgent, but they may still deserve review before they are ignored for years.

The goal is not to rush into decisions. The goal is to separate what needs attention now from what can be reviewed later.

Common job transition situations include:

- Starting a new job with a new benefits package

- Leaving an employer and deciding what to do with an old retirement plan

- Losing employer-provided life insurance or disability coverage

- Being laid off and needing to stabilize household cash flow

- Retiring from an employer and replacing a paycheck with retirement income

- Working past traditional retirement age and deciding when work becomes optional

- Coordinating benefits with a spouse or partner

- Updating beneficiaries after a major life change

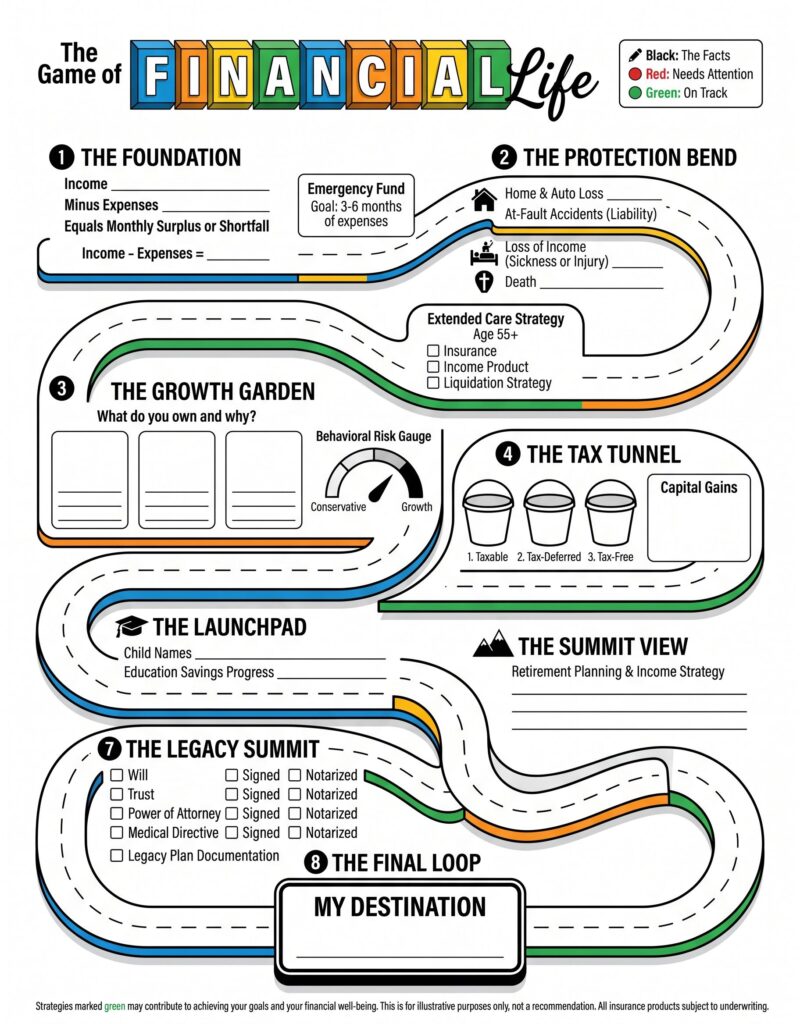

The Game of Financial Life Framework

At Salt Lake Financial Planning, job transition planning is often organized through the Game of Financial Life framework. The framework helps review the major areas of a household’s financial picture in a structured, visual way.

Instead of reviewing one account, one policy, or one benefit in isolation, the framework helps organize how each part of the financial life connects to the others.

1. The Foundation

The Foundation starts with cash flow. During a job transition, the first question is often simple: what income is coming in, what expenses are going out, and what changes when the job changes?

- Income

- Expenses

- Monthly surplus or shortfall

- Emergency fund

- Debt payments

- Final paycheck or severance

- Gap between jobs

- Changes in payroll deductions

For a deeper cash flow review, see Cash Flow Management: Creating a Personal Cash Flow Statement.

2. The Protection Bend

The Protection Bend reviews the risks that may affect the household. During a job transition, this is where employer-provided life insurance, disability coverage, health coverage, and other protection benefits need attention.

- Group life insurance

- Supplemental life insurance

- Short-term disability coverage

- Long-term disability coverage

- Health coverage transition questions

- Home and auto liability exposure

- Extended care or long-term care planning

- Spouse or dependent coverage

For a focused review of group life insurance after employment changes, see Life Insurance After Leaving a Job: Portability vs. Conversion.

For a broader overview of household protection planning, see Are You Properly Prepared for Common Risks?.

3. The Growth Garden

The Growth Garden reviews what investments are owned and why they are owned. During a job transition, this often includes old 401(k), 403(b), 457(b), IRA, Roth, taxable, pension, and employer stock questions.

- Old employer retirement plans

- New employer retirement plan options

- Investment choices

- Fees and expenses

- Risk tolerance

- Pre-tax, Roth, and after-tax balances

- Taxable accounts

- Employer stock or equity compensation

- Account consolidation questions

For old workplace retirement accounts, see What to Do With an Old 401(k) After Leaving a Job.

If you are still trying to locate accounts from prior employers, see How to Find Old 401(k) Accounts.

4. The Tax Tunnel

The Tax Tunnel reviews how different accounts and income sources may be taxed. A job transition may affect withholding, severance, bonuses, retirement plan distributions, Roth versus pre-tax contributions, capital gains, and future retirement income planning.

- Tax withholding

- Severance or bonus income

- Vacation or PTO payout

- Retirement plan distributions

- Traditional versus Roth contributions

- Taxable investment accounts

- Capital gains

- Required minimum distribution questions

- Coordination with a tax professional

For more on investment account tax treatment, see Taxable vs. Tax-Advantaged: Optimizing Your Investment Location.

For rollover tax rules, the IRS provides general information on rollovers of retirement plan and IRA distributions.

5. The Launchpad

The Launchpad focuses on major future goals. During a job transition, this may include education savings, retirement planning, retirement income strategy, and whether the household’s savings pattern still fits the next stage of life.

- Education savings

- Retirement contributions

- Employer match

- Retirement income planning

- Changes in savings rate

- Timing of major goals

- Coordination with spouse or partner benefits

For education planning, see College Savings: Planning for Higher Education in Utah.

6. The Summit View

The Summit View focuses on retirement planning and income strategy. This section becomes especially important when the job transition is retirement or when a person is deciding whether work is still necessary.

- Retirement income needs

- Social Security timing questions

- Pension options

- Retirement account withdrawals

- Required minimum distributions

- Survivor income considerations

- Coordination between income sources

For retirement-specific transition questions, see Retirement Transition Planning: What to Review Before Leaving Work.

For Social Security timing information, the Social Security Administration explains that retirement benefits can start as early as age 62, while delaying beyond full retirement age can increase the benefit amount up to age 70. Review the rules carefully before claiming. See the SSA page on retirement age and benefit reduction.

7. The Legacy Summit

The Legacy Summit reviews estate documents and beneficiary structure. A job transition can reveal outdated beneficiary designations, old employer accounts, prior spouse information, missing powers of attorney, or estate documents that no longer match the household’s current situation.

- Will

- Trust, if applicable

- Power of attorney

- Medical directive

- Retirement account beneficiaries

- Life insurance beneficiaries

- Transfer-on-death designations

- Legacy planning documents

For more on this issue, see Your Estate Plan May Have a Hidden Gap: Why Beneficiary Reviews Matter.

8. The Final Loop

The Final Loop brings the planning conversation back to the household’s destination. The question is not only what changed, but what the household is trying to move toward.

- Desired lifestyle

- Family priorities

- Work flexibility

- Retirement timing

- Debt reduction goals

- Education goals

- Legacy goals

- Planning gaps to revisit

The purpose of the framework is not to make every decision at once. It is to organize the financial picture so the next questions are easier to identify.

Job Transition Decisions That May Have Deadlines

Some job transition decisions may only be available for a limited time. These deadlines vary by employer plan, insurance contract, benefit provider, and individual circumstances.

Items that may have deadlines include:

- New employer benefits enrollment

- Health coverage elections

- COBRA continuation coverage

- Life insurance portability or conversion options

- Retirement plan distribution paperwork

- Pension elections

- Stock option exercise deadlines

- FSA reimbursement deadlines

- HSA contribution questions

- Beneficiary updates for new accounts

The U.S. Department of Labor provides general information on COBRA continuation coverage for workers and families who lose job-based health coverage.

If You Are Starting a New Job

Starting a new job can create a short window of benefit decisions. It can be easy to click through enrollment quickly, but those elections may affect take-home pay, insurance coverage, retirement savings, taxes, and beneficiaries.

Review the new benefits package for:

- Enrollment deadline

- Health plan options

- HSA or FSA options

- Employer retirement plan match

- Traditional versus Roth contribution options

- Group life insurance

- Supplemental life insurance

- Short-term and long-term disability coverage

- Spouse or dependent coverage

- Legal, identity theft, accident, or other voluntary benefits

- Beneficiary designations

- Total paycheck impact

For a detailed benefits enrollment checklist, see New Job Benefits Checklist: What to Review Before You Enroll.

If You Were Laid Off

If you were recently laid off, the first priority is stability. This is usually a Foundation issue before it is an investment issue.

Start by reviewing income, expenses, emergency savings, severance, unemployment income, health coverage, debt payments, and benefit deadlines.

Initial questions to organize:

- How long can current cash reserves support the household?

- When does the final paycheck arrive?

- Is severance available?

- When does employer health coverage end?

- Is COBRA or marketplace coverage available?

- What happens to group life insurance?

- What happens to disability coverage?

- What retirement plan decisions can wait?

- What decisions have deadlines?

- Which expenses should be paused or reprioritized?

For a step-by-step layoff article, see Laid Off? A Financial Checklist for the First 30 Days After Job Loss.

If You Are Leaving an Old Retirement Plan Behind

An old 401(k) or workplace retirement plan should not be ignored. It may be fine to leave assets in a prior employer plan, but that should be a reviewed decision rather than a forgotten default.

Common options may include:

- Leaving the money in the old employer plan, if allowed

- Rolling it into a new employer plan, if the new plan accepts rollovers

- Rolling it into an IRA

- Taking a distribution

Each option has potential advantages, limitations, tax considerations, service differences, investment options, fee structures, and administrative rules.

This article does not recommend one option over another. The appropriate choice depends on the old plan, the new plan, account type, tax status, household goals, service needs, and broader planning context.

For more detail, see What to Do With an Old 401(k) After Leaving a Job.

If You Are Losing Employer-Provided Life Insurance

Many employees have life insurance through work. Some also have supplemental coverage, spouse coverage, or dependent coverage through payroll deduction.

When employment ends, group life insurance may end, reduce, continue for a period, or become available through portability or conversion options. The specific details depend on the employer plan and insurance contract.

Review:

- How much group life insurance was provided

- Whether supplemental coverage was in place

- Whether spouse or dependent coverage was included

- When coverage ends or changes

- Whether portability is available

- Whether conversion is available

- What deadlines apply

- How the cost may change

- Whether the household still has a coverage gap

- Whether beneficiaries are current

For a more specific explanation, see Life Insurance After Leaving a Job: Portability vs. Conversion.

For broader life insurance planning education, see Life Insurance Planning: Protecting Your Family’s Financial Future.

If You Are Retiring From an Employer

Retirement is a job transition, but it is also a larger financial identity transition. The question changes from “How much am I saving?” to “How will my income, benefits, insurance, taxes, and accounts work after employment changes?”

Retirement transition questions may include:

- What income replaces the paycheck?

- What expenses continue, change, or disappear?

- What employer benefits end?

- What pension options are available?

- When should Social Security be reviewed?

- What happens to the employer retirement plan?

- How should pre-tax, Roth, and taxable accounts be coordinated?

- What life insurance coverage continues or ends?

- What long-term care planning questions should be reviewed?

- Are beneficiary designations current?

- Are estate documents current?

- What tax questions should be coordinated with a tax professional?

For the retirement-specific branch article, see Retirement Transition Planning: What to Review Before Leaving Work.

If Medicare is part of the transition, review enrollment timing carefully. Medicare explains that a person generally has up to 8 months after stopping work or losing employer health insurance, whichever happens first, to sign up for Part B without a penalty whether or not COBRA is chosen. See Medicare’s information on COBRA coverage and Medicare.

Questions to Ask Before a Job Transition Review

Before making decisions, it can help to gather the main questions in one place.

Foundation questions:

- What income changes immediately?

- What expenses change immediately?

- How much emergency reserve is available?

- Is there a gap between paychecks?

- Will payroll deductions change take-home pay?

Protection Bend questions:

- What employer-provided insurance ends or changes?

- Is life insurance portable or convertible?

- Will disability coverage continue at the new employer?

- Does the household still have a protection gap?

- Are spouse or dependent benefits affected?

Growth Garden questions:

- What retirement accounts exist?

- Where are old employer accounts located?

- What investment options and fees apply?

- Are accounts coordinated or scattered?

- Does the current investment approach still match the time horizon and risk tolerance?

Tax Tunnel questions:

- Will income be higher or lower this year?

- Should withholding be reviewed?

- Will severance, PTO, bonuses, or distributions affect taxes?

- Are there pre-tax, Roth, and taxable account questions?

- Should a tax professional be involved?

Legacy Summit questions:

- Are beneficiaries current?

- Do old employer accounts still list the correct people?

- Do estate documents reflect the current family situation?

- Are powers of attorney and medical directives in place?

- Should an estate attorney review the documents?

Documents to Gather

A transition review is easier when the major documents are available in one place.

Useful documents may include:

- Old employer benefits guide

- New employer benefits guide

- Severance paperwork, if applicable

- Final paycheck or PTO information

- Health insurance information

- COBRA notice, if applicable

- Group life insurance notice

- Portability or conversion paperwork

- Disability coverage summary

- Retirement plan statement

- Pension estimate, if applicable

- Social Security estimate, if applicable

- Recent tax return

- Recent paystub

- Estate planning documents

- Beneficiary confirmations

- List of monthly expenses

- List of debts

What This Review Does Not Replace

A job transition review can help organize financial questions, deadlines, documents, and planning priorities. It does not replace the role of other professionals or plan-specific resources.

Depending on the issue, additional input may be needed from:

- Human resources

- Employer benefits department

- Retirement plan administrator

- Tax professional

- Estate planning attorney

- Medicare professional or Medicare resources

- Insurance carrier

- Payroll department

The purpose is to identify the right questions and coordinate the planning conversation, not to replace plan documents, legal advice, tax advice, Medicare advice, or employer-specific guidance.

Related Job Transition Resources

- Retirement Transition Planning: What to Review Before Leaving Work

- New Job Benefits Checklist: What to Review Before You Enroll

- Laid Off? A Financial Checklist for the First 30 Days After Job Loss

- What to Do With an Old 401(k) After Leaving a Job

- Life Insurance After Leaving a Job: Portability vs. Conversion

Additional Planning Resources

- What to Expect in Your First Financial Consultation

- When Should You Hire a Financial Advisor?

- How Do Financial Advisors Get Paid?

- Completing the LUTCF® Designation: A Step Forward in Serving Clients

- Key Takeaways From the 2026 NAIFA Utah Symposium

Review Your Transition Questions

A job transition can create several moving parts at once. The review does not need to start with a product decision or a recommendation. It can start by organizing the facts.

Bring benefit paperwork, retirement plan statements, life insurance notices, new employer benefit guides, severance documents, estate documents, and questions that need to be reviewed.

Educational Disclosure

This material is for educational purposes only and is not intended as individualized financial, tax, legal, investment, retirement, health insurance, Medicare, or insurance advice. Employer benefits, retirement plans, insurance options, tax rules, Social Security rules, Medicare rules, and enrollment deadlines vary by plan and individual circumstances. Review your specific plan documents and consult the appropriate professional before making decisions.

Dallas Price is a Financial Planner and offers securities and investment advisory services through LPL Enterprise (LPLE), a Registered Investment Advisor, Member FINRA/SIPC, and an affiliate of LPL Financial.

LPLE and LPL Financial are not affiliated with Salt Lake Financial Planning.