Some events are worth attending because of the information.

Others are worth attending because of the people in the room.

This week’s What’s Working Wednesday had both.

We gathered over lunch for continuing education, conversation, and a presentation from Bart Spencer, a long-time disability income specialist known by many in the industry as “the DI Nut.” That nickname alone tells you something about the room. Bart has spent decades talking about a topic that many financial professionals know is important, but still do not always bring up often enough.

The presentation was called “Seeing the Trees in the Forest: Opportunities to Serve Your Clients with Disability Insurance.”

And that title ended up being the whole point.

In financial planning, it is easy to focus on the visible trees: investments, retirement accounts, life insurance, estate documents, tax planning, business succession, debt, and cash flow.

But Bart kept bringing us back to a larger question:

What keeps the whole financial forest alive?

For many people, the answer is income.

The Room, the Meal, and the Reminder

The setting felt like a classic Utah professional lunch: tables pulled together, handouts on the table, iced tea and water glasses, a projector up front, and a group of advisors and professionals taking time out of the middle of the workday to sharpen the saw.

There was food. There was a pledge. There was some friendly teasing. There was the usual passing around of the CE sheet.

And then Bart got up and did what experienced presenters do best: he turned a technical topic into a human one.

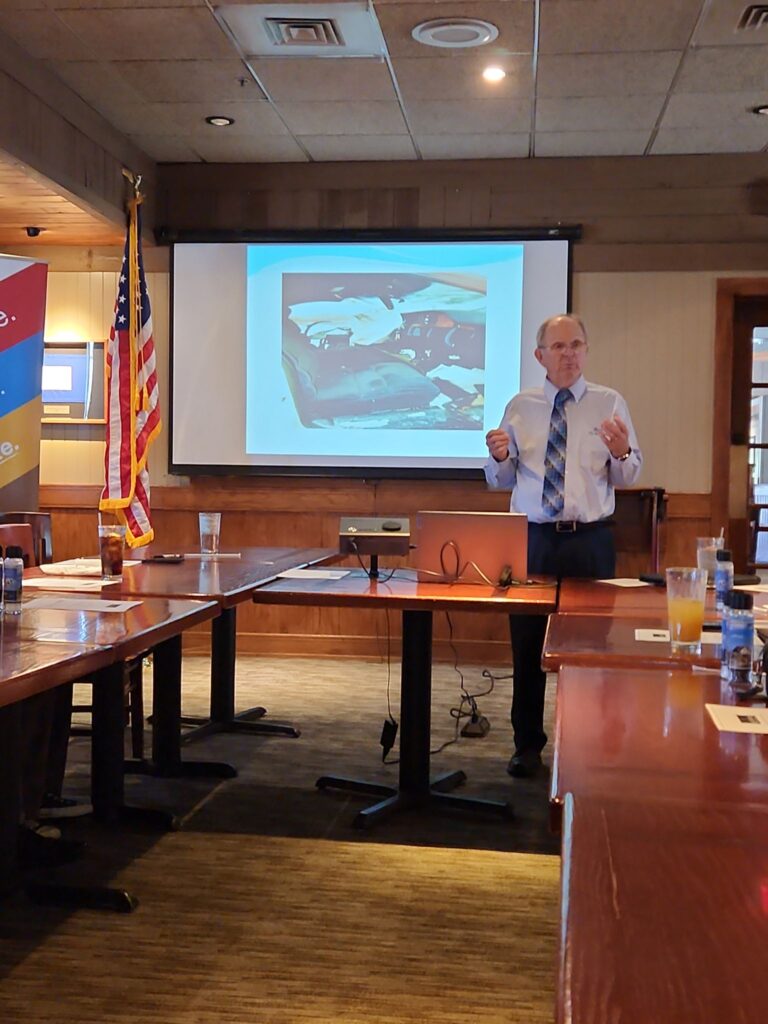

The Case Study That Changed the Room

The most powerful part of the presentation was not a chart or a product explanation.

It was Bart’s own story.

He shared a car accident from January 26, 1996, just south of Lagoon. A truck hauling junk steel crossed the freeway after the driver tried to avoid slowing traffic. Bart was in the passenger seat of the car that was hit.

Bart survived.

His coworker did not.

That story could have gone in several directions. It could have been about life insurance. It could have been about auto liability limits. It could have been about risk management generally.

But Bart used it to ask a deeper planning question.

After the accident, an economic analysis estimated the loss of future employment income at more than $1.7 million. Bart’s point was not just that a person has value after death. His point was that the same earning power also has value while that person is alive.

That is where disability income planning enters the conversation.

A person’s ability to earn may be one of the largest financial assets they have. Yet it is often less visible than an account statement, a home, a business, or a retirement plan.

The Myth: “Social Security Disability Will Take Care of Me”

One of the early discussion points was a common assumption:

“If I become disabled, Social Security Disability Insurance will cover me.”

Bart’s response was direct. That may be part of the safety net, but it is not something most people should treat as their only plan.

The room discussed waiting periods, the claims process, denials, appeals, and the practical reality that households still have to pay bills while everything is being reviewed.

The planning lesson was simple:

A benefit that might help later does not always solve the cash flow problem today.

The Myth: “I Already Have Disability Coverage Through Work”

This was another important takeaway.

Many people have some type of disability coverage through their employer. That can be valuable. But Bart reminded the room that “I have coverage” is not the same as “I understand my coverage.”

A real review should ask:

What percentage of income is covered?

Is it based on salary only, or does it include bonuses and commissions?

Is there a monthly benefit cap?

Are benefits taxable?

How long is the waiting period?

How does the policy define disability?

What happens to other benefits if the person cannot work?

That last point created a strong discussion. One example raised in the room involved a firefighter who went on claim and later received a large bill for family health insurance premiums. The disability benefit was only one part of the picture. The household still had to deal with the broader financial impact.

That is the kind of detail people often miss until they are already in the middle of a difficult situation.

Business Owners Have More Trees in the Forest

For business owners, the conversation gets even more layered.

If an employee cannot work, the concern may be replacing income.

If a business owner cannot work, the concern may also include:

Payroll

Rent

Utilities

Business loans

Staff retention

Client obligations

Accounts receivable

The ability to keep the doors open

Bart talked about business overhead expense coverage, key person planning, business loan protection, and disability buy-sell planning. Those are not everyday dinner-table topics, but they matter for the right businesses.

One of the strongest examples involved dentists and other professional practices. If the doctor or dentist is out for an extended period, the business may still have staff, rent, equipment, and debt. Even if accounts receivable helps for a short time, the pipeline can eventually dry up.

That is where the planning conversation moves beyond “Do you have a policy?” and becomes:

How would the business keep functioning if the key person could not work?

What I Took From the Presentation

The biggest takeaway for me was that disability income is not a side topic.

It connects to almost everything else.

Income funds the mortgage.

Income funds retirement contributions.

Income funds insurance premiums.

Income funds debt repayment.

Income funds college savings.

Income funds the business.

Income funds the plan.

That does not mean every person needs the same strategy. It does mean income should be part of a serious planning conversation.

Bart’s presentation was a good reminder that the best financial professionals do not just look for products. They look for gaps, assumptions, and overlooked risks that could affect a family, a business, or a long-term plan.

A Better Question to Ask

The practical question is not simply:

“Do I have disability insurance?”

A better question is:

“If my income stopped or changed for several months, what would happen first?”

That question can lead to a much more useful conversation.

For some people, the first concern is household cash flow.

For others, it is business overhead.

For others, it is debt.

For others, it is protecting employees or preserving a retirement plan.

That is why “seeing the trees in the forest” is such a useful frame. Each financial decision matters, but the parts are connected.

Grateful for What’s Working Wednesday

I appreciated the opportunity to attend, learn, and connect with other local professionals who care about serving clients well.

A good CE event should do more than check a box. It should make you think differently about the conversations you are having with clients, business owners, and families.

Bart Spencer did that.

And yes, the DI Nut nickname fits.

If it has been a while since you reviewed your income protection, employer benefits, or business continuity planning, it may be worth taking a fresh look.

A planning conversation can help identify what you already have, what you may be assuming, and what questions deserve more attention.

This material is for educational purposes only and is not intended as individualized financial, tax, legal, investment, retirement, or insurance advice. Disability income insurance and related planning strategies may include limitations, exclusions, underwriting requirements, eligibility requirements, costs, and other considerations. Coverage availability and benefits vary by carrier, policy type, occupation, health history, income, employer benefits, and other factors. Review your specific policy, plan documents, and personal circumstances with qualified professionals before making decisions.